The games industry in Flanders (2023)

In 2024, we collected comprehensive data focused on video games. We surveyed 49 game studios on a range of operational factors. Additional input was provided for a total of 37 Flemish video games that received VAF-support and had some form of engagement in 2023.

Our working method

In collaboration with four studios we were able to establish a straightforward declaration system with clear KPIs. We settled on several measuring points including, but not limited to diversity, turnover and game figures.

We contacted all studios that received production support at the very least by 2022 or vertical slice support as of 2023 for one or more projects since the VAF/Game Fund was established. Companies that are no longer primarily focused on games were required to submit a final report on their games and are not included in our 2023 scan. Additionally, companies that are no longer operational have been excluded entirely.

This report includes only games that had some form of engagement in 2023. Given the different business models, the following events count as instances of engagement: downloads, purchases, logins for free to play games and indirect revenue generated through advertising or merchandise. In summary any kind of activity, regardless of revenue is considered to be engagement.

The data collection was limited to Flemish studios that had previously received VAF-support. This corresponds to about 60% of the Flemish market and represents around 30% in terms of revenue. Studios that do not request support from VAF are typically large and generate sufficient revenue to fund their projects independently of financial aid. Our intent is to conduct a more comprehensive survey in collaboration with federations and other relevant bodies in 2024, in order to include these studios in the study.

Latest update: 30/10/2024

Games released in 2023

Games can be released in a number of different ways. The most common way is to release a completed game through one or more distribution channels. In 2023, 12 new Flemish games were released this way, four of which received funding from VAF.

Sometimes a studio or publisher elects to release a game that is not yet complete. This is referred to as a preview version. In many cases in the form of a demo or prototype, where one or more levels are published. This allows the studio to cultivate a loyal community by providing people a look behind the scenes of game development. Moreover, the team receives valuable feedback, which enables them to make changes to the game in collaboration with their fans. In some instances, the creator sells the consumer the unfinished game, usually at a discount. This method is commonly referred to as 'Early Access' or 'Paid Alpha' within the industry and allows the studio to rely on an (additional) revenue stream to complete the game while engaging its loyal community in the development process and collecting feedback. Consequently, these players are designated as ambassadors, provided with updates and eventually the full completed game. In the previous year, one game that had received VAF-support was made available in a trial version, where the game was released as a free prototype.

A third pillar of releases we labelled ‘re-release'. Games are typically developed on a single platform and subsequently adapted for other platforms. Games developed for PC will not work on PlayStation or Nintendo Switch by default; this requires meticulous adaptation and in some cases a complete overhaul of the software. This can be very costly, but could reach a previously untapped audience, which is why it's recognized as an additional release, provided the original game was released in another year. In Flanders, three games appeared as ‘re-releases’ in 2023, one of them with VAF-support.

The fourth and final major category is expansions, which could include additional levels, gamemodes, items or story. It should be noted that this is different from a sequel. A sequel is a stand-alone game that can be purchased separately and played independently of the original game. An expansion, on the other hand, marketed as 'downloadable content' (DLC for short), 'season pass' or 'expansion', can usually only be played if you own the original game. No expansions were released in Flanders in 2023.

Why we don't publish individual game figures

In light of the sensitive international and competitive context, we have chosen not to release individual figures. Given that games are released globally, where the market is dominated by a handful of major players, publishing figures of Flemish studios could put them at a disadvantage. Only aggregated turnover figures are published.

Furthermore, we can't provide accurate and comparable numerical data. Some games are monetised through subscription formulas, while other titles are free-to-play and generate revenue from advertisements or expansions. This makes it near impossible to make an accurate comparison between these figures, without a way to process and normalise these figures.

Turnover by category

In 2023, 37 VAF-supported games generated revenue. A closer examination of sales from these games reveals that the majority of these sales were generated by entertainment games. This is logical, given that entertainment games theoretically sell for up to 79 euros per copy for titles in the 'AAA segment', whereas educational games typically limit purchases to one copy per school, or sometimes even offer them for free. This is why cultural and social value are equally important as sales figures.

| Category | Number | Turnover |

|---|---|---|

| Entertainment | 29 | 10 065 254 EUR |

| Artistic | 3 | 49 729 EUR |

| Educational | 3 | 35 986 EUR |

| Serious | 2 | 356 145 EUR |

| Total | 37 | 10 507 114 EUR |

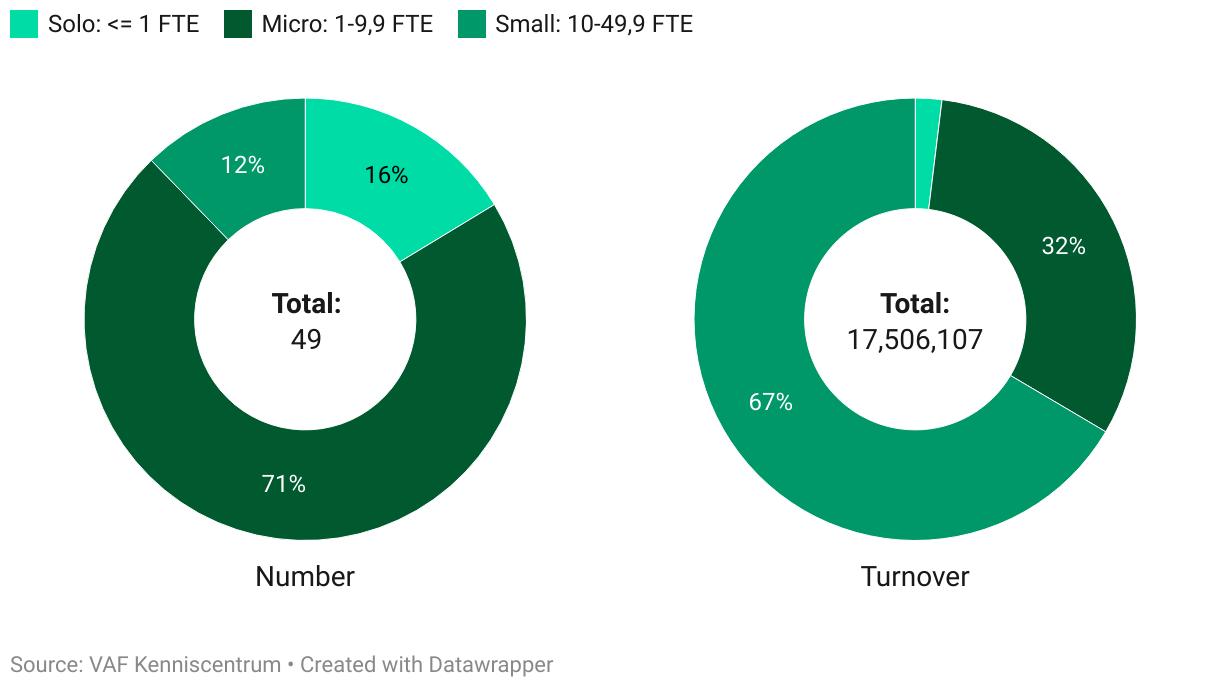

Turnover of game studios

A review of the aggregated business turnover of the 49 studios that participated in our survey indicates a total of € 17.5 million in 2023. A total of 22.3% of the turnover is accounted for by ‘work for hire’ which indicates that the revenue was generated from work for third parties, rather than from the studio's intellectual property. It is crucial for many studios to guarantee a consistent revenue stream, given that it takes approximately two to three years for a game to be released, with outliers due to the complexity of the game itself, interruptions due to other projects or ‘work for hire’.

In 2022, the total operating turnover of these studios was € 14.7 million, representing a year-on-year increase of 2.8 million. The proportion of 'work for hire' was significantly higher in 2022 at 32.3% but dropped by 10 percentage points in 2023.

The growth in total turnover and the decrease in the proportion of work-for-hire are both indications that the sector is becoming more robust and stable.

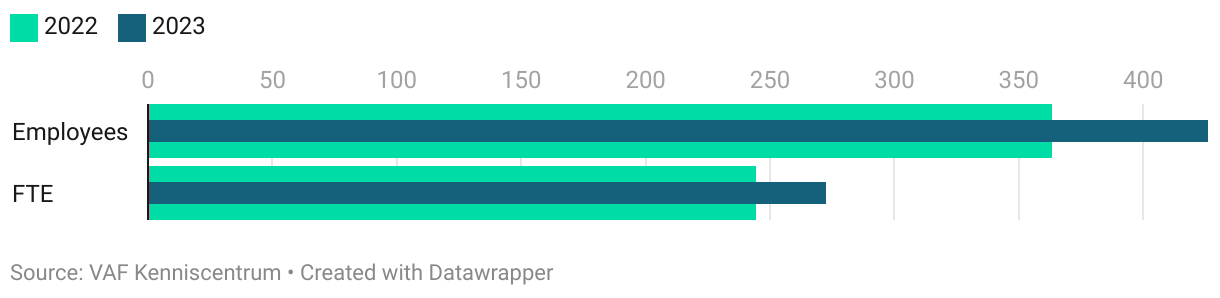

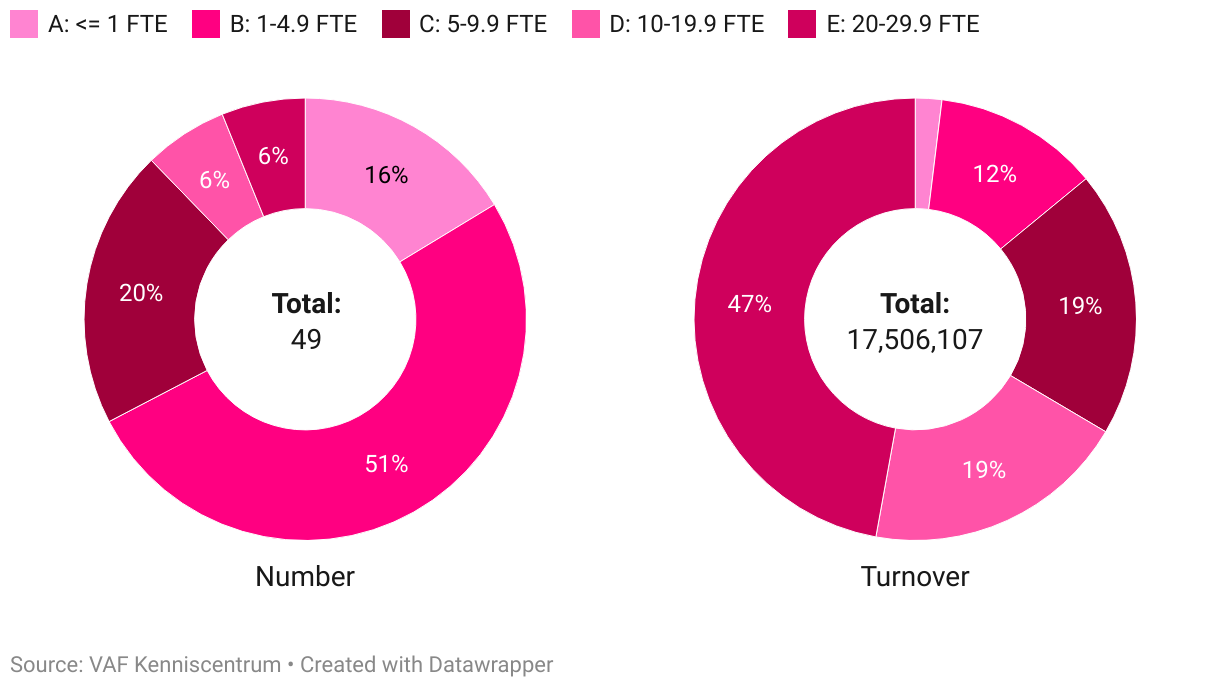

Total number of employees

A total of 46 studios took part in this study and supplied data for both 2022 and 2023. Three studios were only established last year and therefore unable to provide figures for 2022. The table below provides a year-on-year comparison of the number of studios, employees and full-time equivalents (FTE’s), including the share of the three new studios. The number of employees increased by 17.4% year-on-year, while the number of full-time equivalents rose by 11.8%.

| 2022 | 2023 | Difference | Share new studios | |

|---|---|---|---|---|

| Studios | 46 | 49 | +3 | 3 |

| Employees | 363 | 426 | +63 | 15 |

| FTE* | 243,95 | 272,82 | +28,87 | 7,20 |

*FTE= Full-time equivalents

Who are the employees?

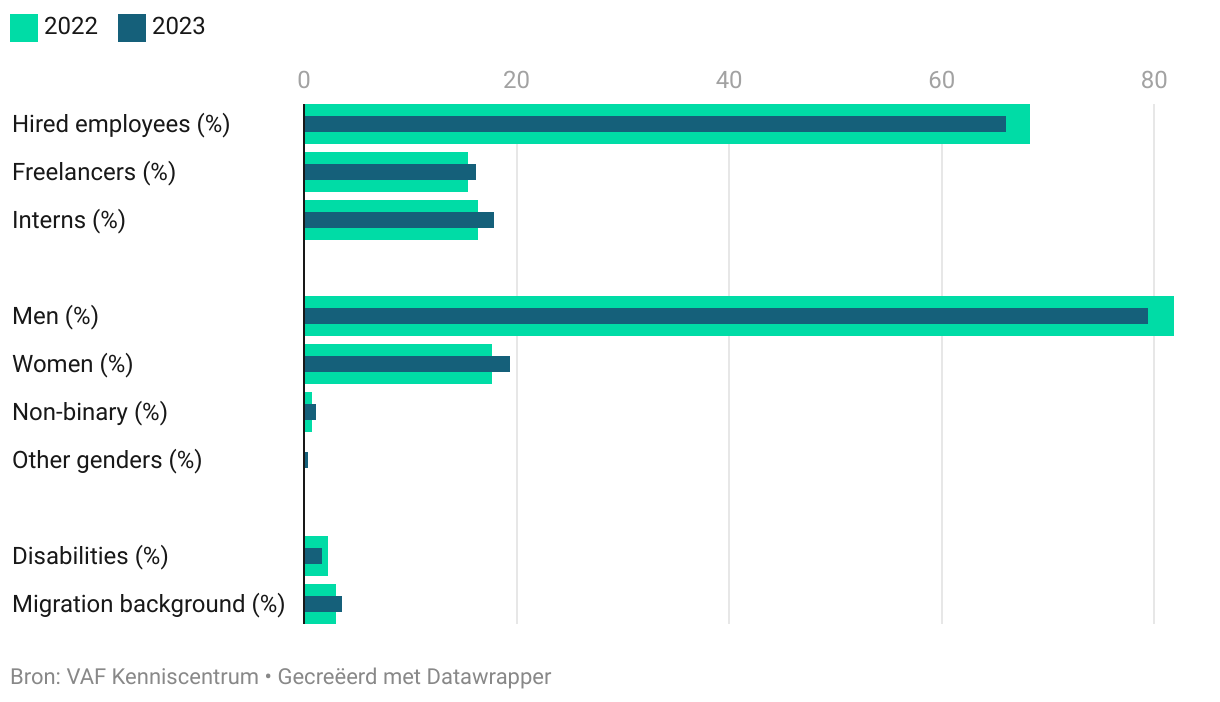

We requested additional details from the studios regarding the composition of their teams and were able to determine that the percentage of permanent employees declined slightly in 2023, from 68.3% to 66%. The number of freelancers increased from 15.4% to 16.2%, while the number of interns rose from 16.3% to 17.8%. These changes are not significant enough and understandable given that many start-up studios require temporary support. The sector still requires a high amount of flexibility.

When we take a closer look at gender, there are encouraging trends. For example, the percentage of women increased from 17.6% to 19.3%. It is worth noting that this percentage is higher than the proportion of women graduates in game education in 2023 (Howest DAE and LUCA), where the figure stands at just 16.7%. Despite these figures, there is a clear need for further improvement in terms of gender balance. It remains a distinctly male-dominated world, particularly when compared to the percentage of women represented in the roles VAF monitors in its application files. The proportion of women in the roles of game director (3% of those involved in VAF application files) and technical director (4%) is very low. It is noteworthy that the percentage for the role of art director is significantly higher (23%). There has been an increase in the number of non-binary individuals in the sector, from 0.7% to 1.1%. Additionally, in 2023, 0.3% of individuals identified as a gender not included in our survey, compared to none in 2022. We will continue to monitor these developments in the coming years.

The proportion of employees with disabilities, including neurodiversity, increased from 1.6% in 2022 to 2.2% in 2023. There was a slight decrease in the percentage of employees with a migration background according to the VESOC definition*, from 3.5% to 3.3%.

* In accordance with the VESOC definition, the term 'third country national' refers to an individual who possesses the nationality of a country outside the EU-15, or an individual with at least one parent or two grandparents who hold the nationality of a country outside the EU-15.

Education

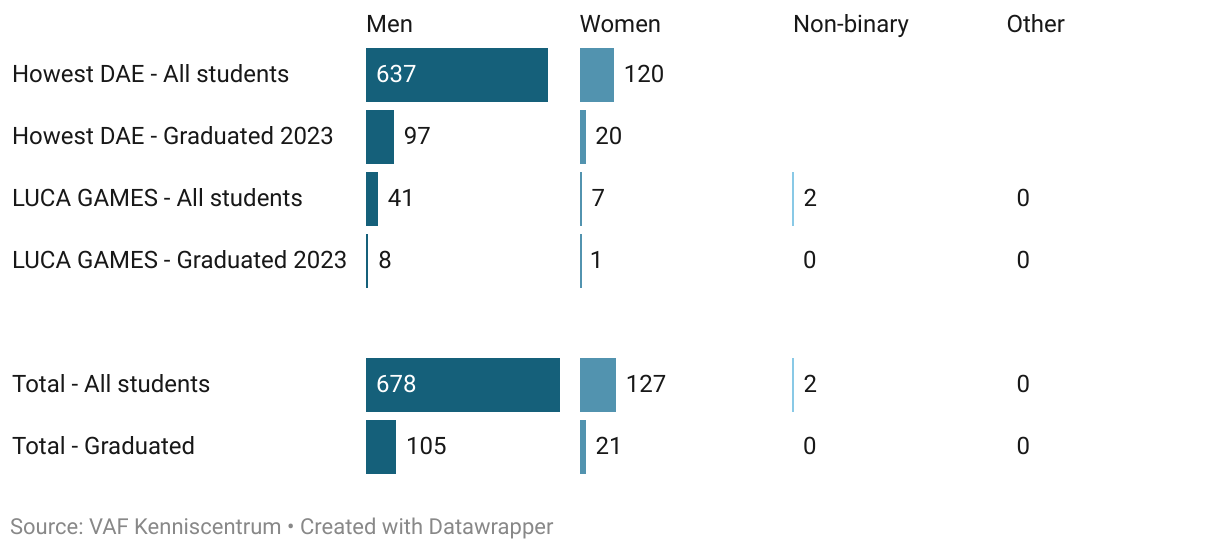

In regards to gender the demographic profile of university students can be considered an indicator of the future composition of employees. Two bachelor degrees are available in Flanders and Brussels with a focus on video games: Digital Arts & Entertainment (DAE) at Howest in Kortrijk and Game Design at LUCA in Genk. The former offers an English-language curriculum, while the latter is in Dutch-language. Both are open to international students and offer shorter programmes for one or more semesters in addition to the three-year bachelor's degree.

The graph below provides a detailed analysis of the Belgian students enrolled in these two programmes, with a particular focus on the total number of students and the number of students graduating in 2023 who will most likely represent the new employees of Flemish game studios in 2023. At Howest, 15.9% of registered students were women. However Howest does not possess data regarding non-binary individuals or any other genders besides men and women. Notably, international students account for nearly twice the proportion of women students. When including them in the calculation, the percentage of women students rises to 24.5%.

At LUCA, we see that 14% of the total number of students are women, 4% are non-binary and 82% identify as men. Here, we also see that international students provide a higher proportion of women. If we include them, it is 19.3% women and 3.5% non-binary.

Among 2023 graduates of DAE, 17.1% were women (out of 117 students). Graduates of Game Design, 11.1% were women (out of 9 students). This means that collectively 16.7% of game education graduates were women.

This is expected to increase further in the coming years. Overall, the number of women among new students in 2023 increased (18.3%). The games industry remains male-dominated, but it is encouraging to see that women are increasingly represented in the workforce.

Geographically: Provinces

Looking more closely at the data the geographical distribution of the 49 participating studios are interesting to say the least. East-Flanders scores highest overall in terms of number (17 studios), turnover (EUR 8.6 million) and employees (100 FTE). However, Antwerp has the best ratios, with an average of 8.18 FTE per studio and a turnover of EUR 545 000 per studio. East-Flanders, on the other hand has the best turnover per FTE (EUR 88K).

| Province | Avg. FTE per studio | Turnover per studio | Turnover per FTE |

|---|---|---|---|

| East Flanders | 5,9 | 518.037 EUR | 88.066 EUR |

| Antwerp | 8,2 | 545.033 EUR | 67.080 EUR |

| Limburg | 4,6 | 284.494 EUR | 61.465 EUR |

| Flemish Brabant | 7,5 | 186.387 EUR | 24.852 EUR |

| Brussels | 4,3 | 171.095 EUR | 39.790 EUR |

| West Flanders | 2,3 | 80.049 EUR | 34.804 EUR |

Turnover per province

Wanneer werd AI geb

FTE per province

Bedrijfsgrootte

Bedrijfsgrootte, aangepaste schaal

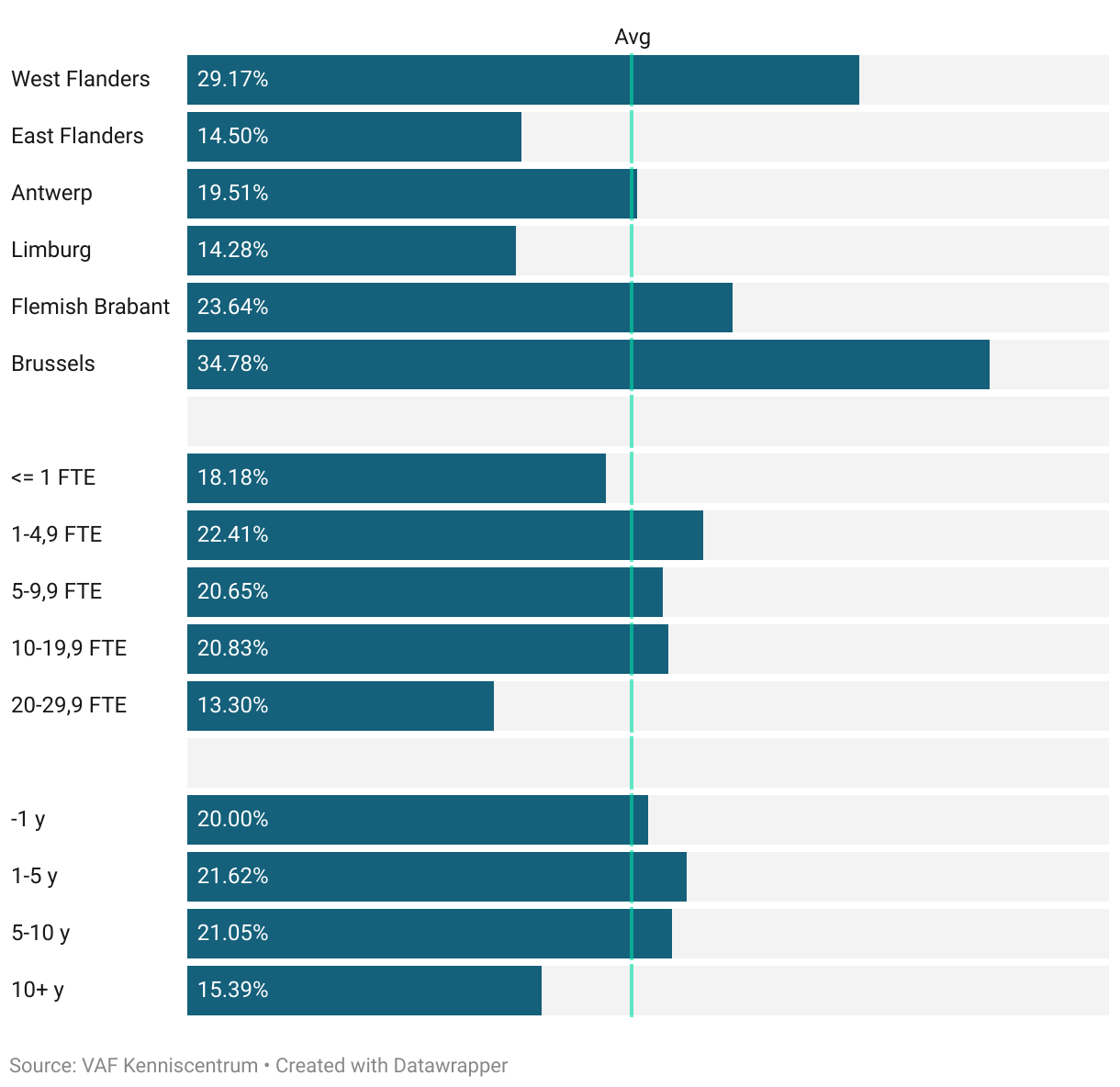

Work for hire: additional observations

As mentioned before, 22.3% of total income came from 'work for hire'. This means that revenue was generated from work for other companies, not from their own intellectual property. It is important for studios to have a stable revenue stream while working on their game, since it can take two to three years for a game to see the light of day.

If we analyse how much 'work for hire' is done by province, there are some interesting findings. In West Flanders, 'work for hire' is double than the average (48.2%), presumably because of training and incubators. Limburg (16.5%) is one of the lowest-performing provinces in 2023. Only beaten by Antwerp with only 12.9% of turnover originating from 'work from hire'.

Surprisingly, ‘work for hire’ in the youngest and smallest studios is very low; only 8.8% of the turnover of studios with less than 1 FTE and 10.4% of the turnover of studios less than 1 year old. We presume that they may rely on funding such as VAF-support for the first year, or that the founders may still be employed elsewhere and are therefore have a stable income while they're working on game projects that don't generate income.

Studios between 1 and 5 years old are pretty close to the average (24.9%). However, just one category higher - studios between 5 and 10 years old - a spectacular 60% of turnover comes from 'work for hire'. These studios have usually built up a sizeable team. We can see this represented in the increase of average number of FTEs. Since they have more employees who need a steady source of income but the studio's games might not generate enough income to bridge the development periods, they need to look for income elsewhere. Once a sufficient buffer has been built up, this percentage drops to 51.5% in the next age category (10+ years). We see similar trends in terms of number of employees, where 42.8% of revenue comes from 'work for hire' in studios with 1 to 4.9 FTE, and then decreases again.

It is noteworthy that the largest studios (20-29.9 FTEs: 28.5%) still rely on this source of income. Do these percentages reflect the balance that experienced studios have reached in order to continue to grow? Are these practical solutions to keep everyone working and not have downtime at various stages of game development. Or could we see this as a sign that companies are struggling, due to growing pains or an ever-changing market? These findings call for further research and a single snapshot is not enough to draw a definitive conclusion.

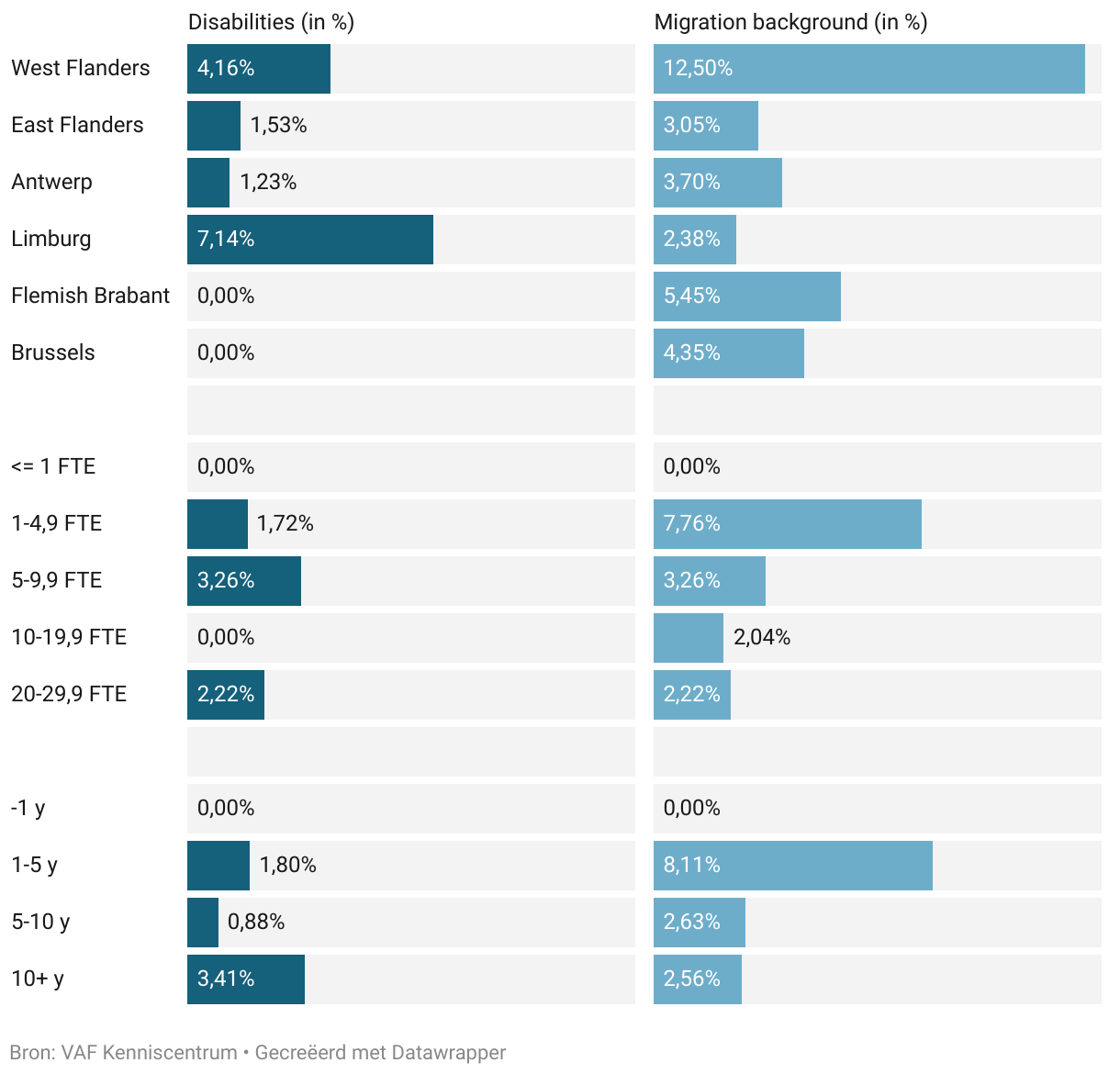

A broader view on diversity

Diversity is more than gender. Limburg and West Flanders have the highest percentages of employees with a disability, in which we specifically included neurodiversity. The fact that these two provinces are also home to the only game courses in Flanders may have an influence on these results. Game studios in Flemish Brabant and Brussels do not have any employees with reported disabilities.

In West Flanders, where Howest is the only university in Flanders to also offer courses in English, we see that no less than 12.5% of the employees have a migration background, although in absolute terms this is only 3 out of 24 employees so our sample size is too small to make definitive conclusions. Limburg, on the other hand, has the lowest proportion of employees with a migration background, with only 1 out of 42 employees or 2.38%.

An interesting trend we noticed is that younger and smaller companies have more employees with a migration background. 7.76% of employees in a studio with between 1 and 4.9 FTEs have a migration background. The same is true for 8.11% of employees in studios between 1 and 5 FTEs. Larger and older companies on average employ fewer people with a migration background. The younger or smaller the company, the more opportunities may be given to someone with a migration background.

People with disabilities are pretty evenly represented in most segments. However, companies with 10 to 19.9 FTE had no people with disabilities in 2023, which we believe is mere happenstance and not indicative of certain trends. We can see that the more employees with disabilities work in the older and more established studios: employees with disabilities in the 10+ category is relatively high (3.41%).

What is most remarkable, is that studios with up to one full-time equivalent (FTE) – which includes the owners – do not have any employees with a disability or migration background. In general, these are sole proprietorships. This observation does not imply that there are no founders without a migration background or disability; rather, such individuals are more likely to be found in younger studios with multiple founders.

Remarks

- In accordance with the terms of the contract, each game studio that receives VAF- support is required to provide annual numerical data for as long as it is still operating. Under those contractual terms, we requested these data in 2023.

- With regards to the composition of the teams, we requested only aggregated figures, limited to the extent of the information available. No individual personal data were received.

- The final revenue figures are not yet known, as the financial statements have yet to be prepared. Therefore, we permitted the studios to enter their latest forecast.

- In Belgium, 100 studios are currently operational, with a total turnover of €65.5 million (source: Belgian Games, 2022). It is estimated that approximately 80 studios are in business in Flanders and Brussels. Thus, this study encompasses approximately half of all Belgian studios and two-thirds of all studios in Flanders and Brussels.

- It is important to note that the target group in our study is not necessarily representative of the entire industry. It does illustrate a number of significant trends. VAF attracts both new and experienced studios. However, some studios have been operating for a longer period and have never been eligible for VAF-support, as they were already financially independent at the time of the founding of the VAF/Game Fund. For instance, Larian Studios employed 81.7 full-time equivalents (FTEs) in Belgium in 2022 (source: 2022 annual accounts) and 470 employees worldwide (source: interview). The most recent game released by the company, Baldur's Gate 3, generated over $600 million in revenue (source: Twitter/X). These figures are not included in this study.

- The studios receive many surveys and have been advocating for more efficient ways to collect data. We are discussing a collaboration with the game associations and other stakeholders to organize a collective scan per year. This will lead to more willingness to share information and less work for the studios.